Educational only. Not financial advice. Past performance is not indicative of future results.

DCA S&P 500 COVID crash 2020 — the fastest bear market in U.S. equity history, and the fastest recovery. Peak to −34% in 33 days, full recovery in roughly five months. This article runs a real dollar-cost average through the entire 2020 window and shows exactly what happened to the money — because the speed of this particular cycle made the usual DCA vs. lump-sum debate behave in a counterintuitive way.

What would DCA into the S&P 500 during 2020 have returned?

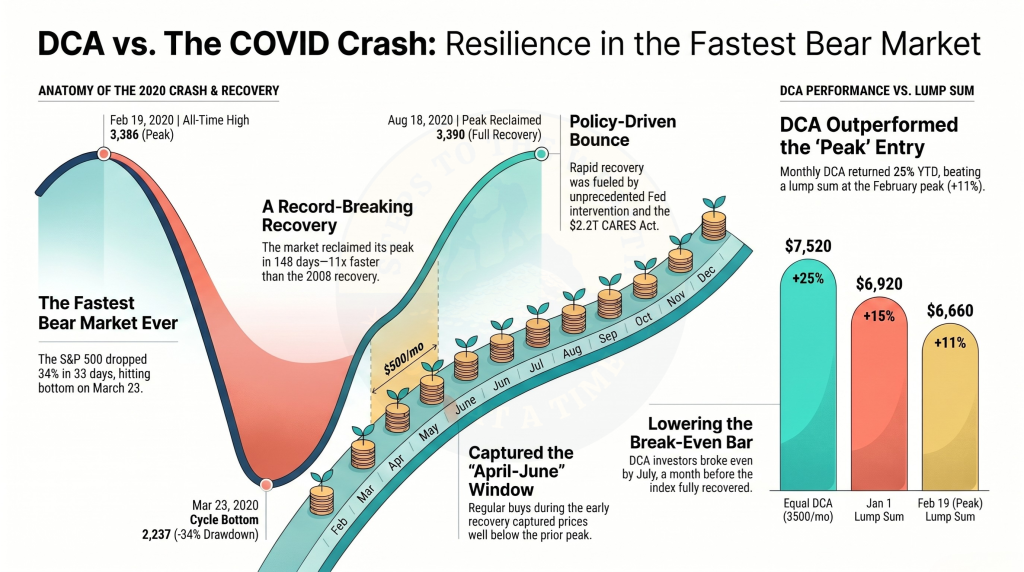

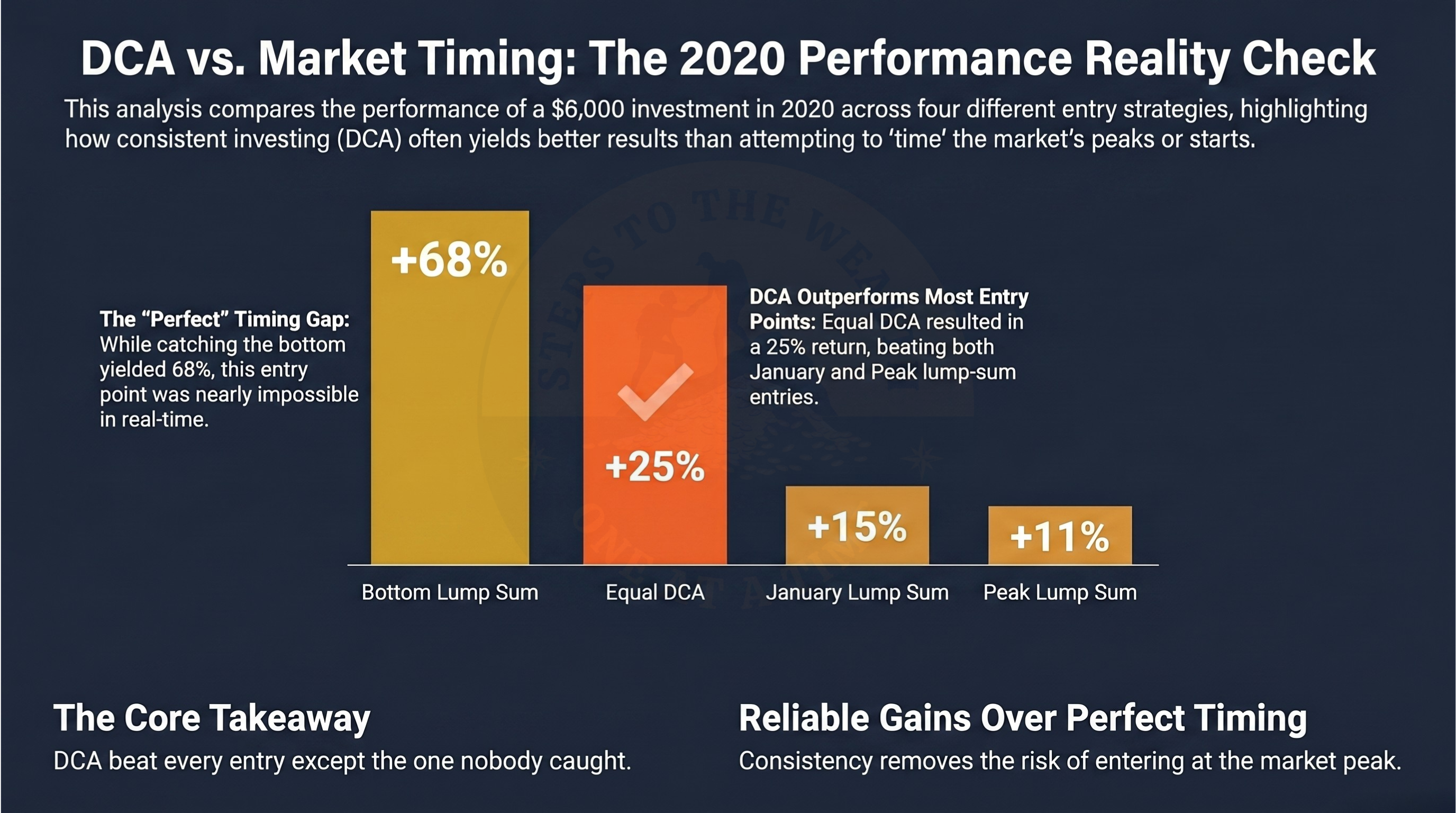

A $500-per-month equal DCA into the S&P 500 from January 1, 2020 through December 31, 2020 — $6,000 invested total — would have ended the year worth approximately $7,520. A gain of roughly 25%, driven by three specific buys (April, May, and June) that landed while price was still well below the February peak but while the eventual recovery was already underway.

This is a better result than the same investor would have gotten from a lump sum on January 1, 2020, and dramatically better than a lump sum at the February peak. It is of course far worse than a lump sum at the March 23 bottom — but nobody knew March 23 was the bottom when they were standing in it.

The outcome is a clean example of DCA’s core design goal: reduce the variance of outcomes around timing, at the cost of giving up best-case returns.

How deep was the COVID stock market crash?

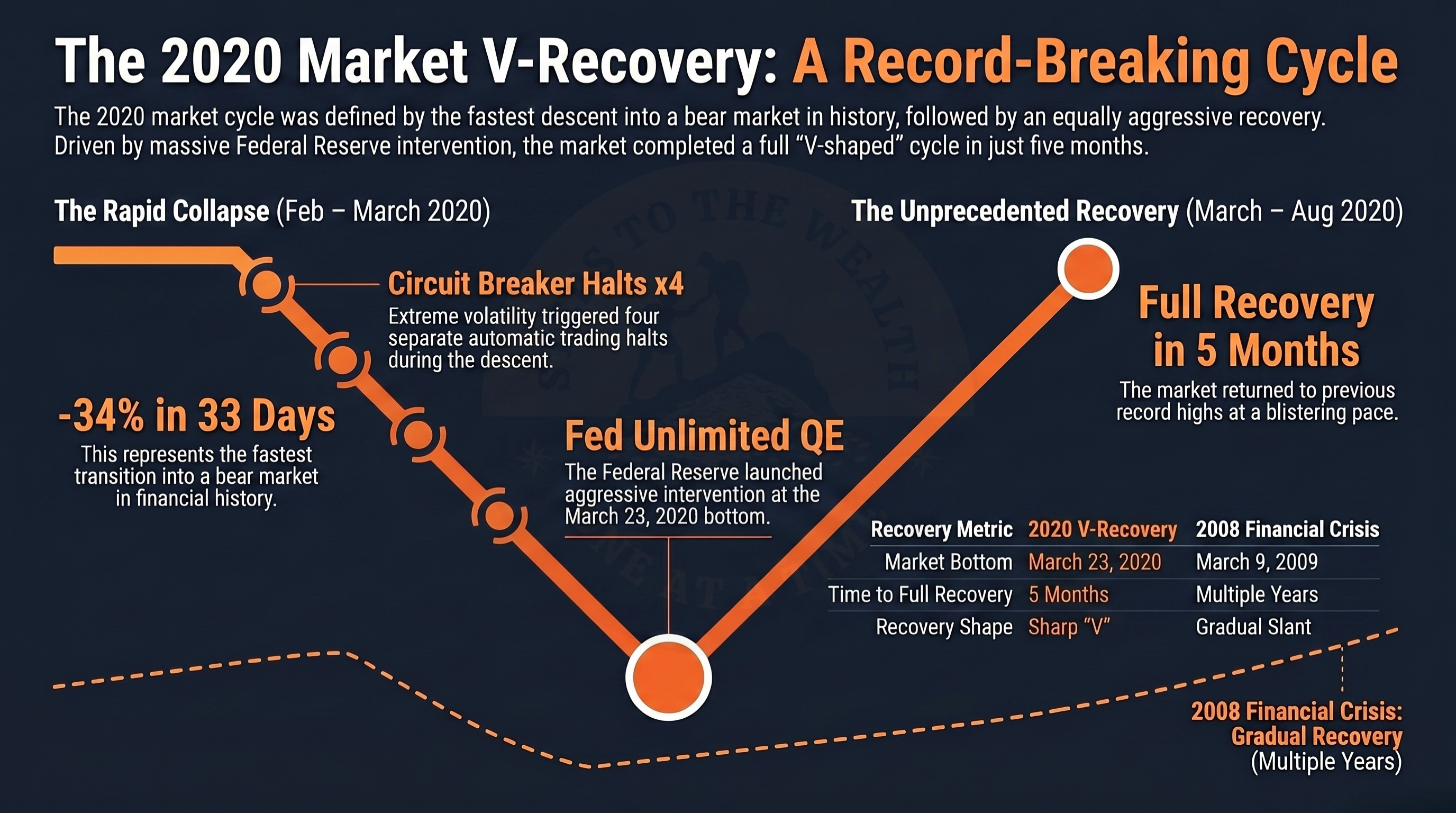

The S&P 500 peaked at approximately 3,386 on February 19, 2020 and bottomed at approximately 2,237 on March 23, 2020 — a drawdown of roughly 34% in just 33 calendar days. It crossed the official bear-market threshold (a decline of 20% from peak) on March 12 after only 16 trading days, the fastest bear market in U.S. equity history by that measure.

Key dates inside the window:

| Date | S&P 500 Close (approx.) | Event |

|---|---|---|

| Feb 19, 2020 | 3,386 | All-time high (at the time) |

| Mar 9, 2020 | 2,746 | First circuit-breaker halt; oil price war |

| Mar 12, 2020 | 2,481 | −20% crossed — fastest ever |

| Mar 15, 2020 | — | Fed emergency cut to 0–0.25%; QE resumed |

| Mar 23, 2020 | 2,237 | Cycle bottom; Fed announces unlimited QE |

| Apr 1, 2020 | 2,471 | Recovery base |

| Aug 18, 2020 | 3,390 | Feb peak reclaimed (148 days from bottom) |

| Dec 31, 2020 | 3,756 | End of measurement window (+11% YTD from Jan 1) |

The crash was driven by genuine shock — an unprecedented global shutdown, with earnings expectations rewriting themselves weekly. The recovery was driven by the fastest and largest monetary and fiscal response in modern history. Neither was knowable in real time.

Did DCA beat lump sum during the COVID crash?

Equal DCA across 2020 beat every lump-sum deployment except the one at the March 23 bottom. The speed of the recovery — and the fact that it began before anyone realized the crash was over — made the lump-sum-wins-two-thirds-of-the-time historical average temporarily not apply to this specific cycle.

- Equal DCA, $500/mo Jan–Dec → ~2.00 index units → approximately $7,520 on December 31 (+25%)

- Lump sum on January 1, 2020 at 3,257 → ~1.84 units → approximately $6,920 on December 31 (+15%)

- Lump sum on February 19, 2020 at 3,386 (the peak) → ~1.77 units → approximately $6,660 on December 31 (+11%)

- Lump sum on March 23, 2020 at 2,237 (the bottom) → ~2.68 units → approximately $10,070 on December 31 (+68%)

DCA beat peak lump sum by 14 percentage points here. That is not the usual historical pattern — and it happened specifically because the crash was short enough and recovery fast enough that DCA’s spread-the-risk mechanic captured the full dip without getting buried in extended drawdown.

Why did the S&P 500 recover so fast from COVID?

The S&P 500 recovered in approximately five months primarily because the policy response was immediate, coordinated, and unprecedented in scale. The Fed cut rates to 0–0.25% on March 15, announced unlimited quantitative easing on March 23 (the day of the bottom), and expanded its balance sheet by roughly $3 trillion within three months. Fiscal stimulus — the $2.2 trillion CARES Act — was signed March 27.

- Monetary response. Rate cuts and unlimited QE established a floor under risk assets within two weeks of the bear-market threshold.

- Fiscal response. $2.2T CARES Act plus subsequent supplemental stimulus materially supported consumer demand and corporate balance sheets.

- Earnings snap-back. Tech, e-commerce, and digital infrastructure names saw accelerated demand, lifting index earnings faster than the real economy.

- No banking crisis. Unlike 2008, there was no systemic financial plumbing failure. The shock was exogenous (a virus) and the transmission mechanism stayed intact.

This matters for how you should generalize the COVID outcome: it was a shock-and-response cycle, not a structural bear market. Applying the recovery speed of 2020 to a future crash with different causes is a mistake. The 2008 precedent, where recovery took 5.4 years, is equally relevant.

How does equal DCA compare to dynamic DCA through the COVID crash?

Dynamic DCA would have outperformed equal DCA in the 2020 window, but by a smaller margin than in slower crashes. The speed of the recovery compressed the window in which dynamic DCA’s risk signals could actually fire.

- Through January and early February 2020: Risk readings were High (elevated valuation, bullish sentiment). Dynamic DCA would have reduced or paused buys. Equal DCA kept buying at 3,200+.

- Late February through March: Sentiment collapsed, valuations compressed. Risk readings rolled to Low by mid-March. Dynamic DCA would have scaled up buys 2x or 3x standard.

- April through July: Risk readings stayed Medium-to-Low as price recovered. Dynamic DCA would have sized up buys into the first two months of recovery.

- August onward: Risk readings climbed back to Medium/High as the index made new highs. Dynamic DCA would have tapered.

The catch: dynamic DCA requires a framework that fires risk readings in near-real time. In March 2020, most risk signals were firing Low — but most investors were paralyzed. The engine is only as good as the operator’s willingness to execute the oversized buys the framework calls for. In a 33-day crash, there are only three or four scheduled buy dates inside the sharpest drawdown. Missing even one is expensive.

How long did it take the S&P 500 to recover from the COVID crash?

The S&P 500 reclaimed its February 19, 2020 peak on August 18, 2020 — approximately 148 days from the March 23 bottom, or just under five months from peak to reclaim. For comparison, the 2008 bear market took 5.4 years to reclaim its prior peak. COVID was roughly 11x faster.

For the DCA investor, break-even happened even earlier — by mid-to-late July 2020 on total-return basis — because the cost basis accumulated across January through June was lower than the January 1 starting price. Each buy in April, May, and June landed below 3,150 and pulled the average down materially.

This is the asymmetry that makes DCA through a fast crash surprisingly profitable: the investor didn’t need the index to reach the prior peak to break even. They only needed price to cross the average cost basis.

Should you keep investing during a fast crash?

Whether you should keep investing during a fast crash depends on the same four things that govern any crash decision: time horizon, financial stability, thesis integrity, and pre-committed plan. Fast crashes add a fifth consideration: recovery can outrun your decision-making speed. By the time you feel comfortable buying again, the window is usually closed.

- Don’t wait for confirmation. In 2020, “confirmation” that the crash was over came in August. The bottom was in March. Anyone waiting for the all-clear missed the recovery entirely.

- Use the scheduled buy as the default action. If your plan says buy on the 1st of the month, and the 1st arrives during a crash, the default action is to execute — not to pause and reassess. Pauses during fast crashes are almost always wrong in hindsight.

- Scale up if your framework supports it. If you run dynamic DCA and your risk readings roll to Low, the whole point of the system is to buy more at that point. Not less. Not the same. More.

- Don’t over-learn from 2020. The COVID recovery was historically fast because the policy response was historically aggressive. The next crash might behave like 2008, or like 1973, or like something that hasn’t happened before. Your plan should work across multiple cycle shapes, not be optimized for one.

Run this scenario with your own numbers

The $500/mo baseline above is illustrative. Your plan is probably different — different starting month, different contribution amount, different end date, different strategy.

DCA Simulator Pro lets you run this exact scenario with your own inputs, compare equal vs. dynamic DCA head-to-head, and replay the COVID crash at different buy cadences (weekly, bi-weekly, monthly) to see how frequency affected outcome. It also covers the 2008 GFC, the 2022 Bitcoin crash, and the dot-com bust for comparative testing.

More crash scenarios

- DCA Into the S&P 500 Through the 2008 Financial Crisis — 57% drawdown over 517 days. The opposite of COVID: slow, structural, and five years to recover.

- DCA Into Bitcoin From 2021 Through the 2022 Crash — 77.5% drawdown, three contagion events (LUNA, Celsius/3AC, FTX), 38 months to break even.

FAQ

What was the lowest S&P 500 price during the COVID crash?

The S&P 500’s cycle low was approximately 2,237 on March 23, 2020, reached the same day the Federal Reserve announced unlimited quantitative easing. Intraday lows on some sessions in March printed below 2,200; the 2,237 figure refers to daily close.

How long did the COVID bear market last?

The COVID bear market officially ran from the February 19, 2020 peak to the March 23, 2020 bottom — 33 calendar days, or 23 trading days. It is the shortest bear market in modern S&P 500 history. The prior peak was reclaimed on August 18, 2020, giving a full peak-to-peak cycle of approximately six months.

Is DCA better than lump sum for the S&P 500?

Across all historical rolling windows, lump sum beats DCA approximately two-thirds of the time on expected value (Vanguard, 2012). DCA reduces the variance of outcomes — better worst-case, worse best-case. The COVID crash was an exception where DCA beat most lump-sum timings inside the single calendar year, specifically because the crash was short and the recovery fast.

How much would $100 per month have been worth after DCA through 2020?

Approximately $1,500 on $1,200 invested, using the same cost-basis logic as the $500 per month example. A gain of roughly 25% by December 31, 2020.

What is a circuit breaker in the stock market?

A circuit breaker is an automated trading halt triggered when an index drops by a specific percentage in a single session. The S&P 500 has three levels: Level 1 at −7%, Level 2 at −13%, and Level 3 at −20%. Level 1 and Level 2 trigger 15-minute halts; Level 3 halts trading for the rest of the day. Four Level 1 halts fired during the COVID crash (March 9, 12, 16, and 18) — the first time circuit breakers had triggered since 1997.

Educational only. Not financial advice. Nothing in this article is a recommendation to buy, sell, or hold any asset. Past performance is not indicative of future results. Do your own research.